Earlier this month, we published a piece in Trellis on how to fund methane reductions at scale—a financing and policy roadmap for biowaste. That article laid out the “what” and the “why.”

This article is about the “how”—the credit architecture that connects one phase of that roadmap to the next, from catalytic carbon finance to durable recycling funding—that can be introduced anywhere.

The Challenge

Biowaste represents approximately 50% of global waste, yet less than 2% is biologically treated despite it being nearly 100% recyclable. Methane gas that is released from food scraps, green waste, sludge, manure and other organic residues that biodegrade anaerobically (without oxygen) in landfills, dumps, and wastewater pools represents approximately 25% of total global methane emissions—a potent greenhouse gas responsible for an estimated one-third of current global warming.

The gap is not a technology problem. The solutions exist and are proven: composting, anaerobic digestion, and insect and microbial processing. Diverting biowaste from landfills and dumps not only prevents methane at its source, but treating them produces valuable products: organic fertilizer, green power, and proteins, along with creating important local impacts such as healthier soils, cleaner and healthier communities, and green jobs.

Incredibly, only 1% of waste-derived methane abatement funding has gone to biowaste treatment (Climate Policy Initiative).

The challenge is well understood. The bottleneck has been market design.

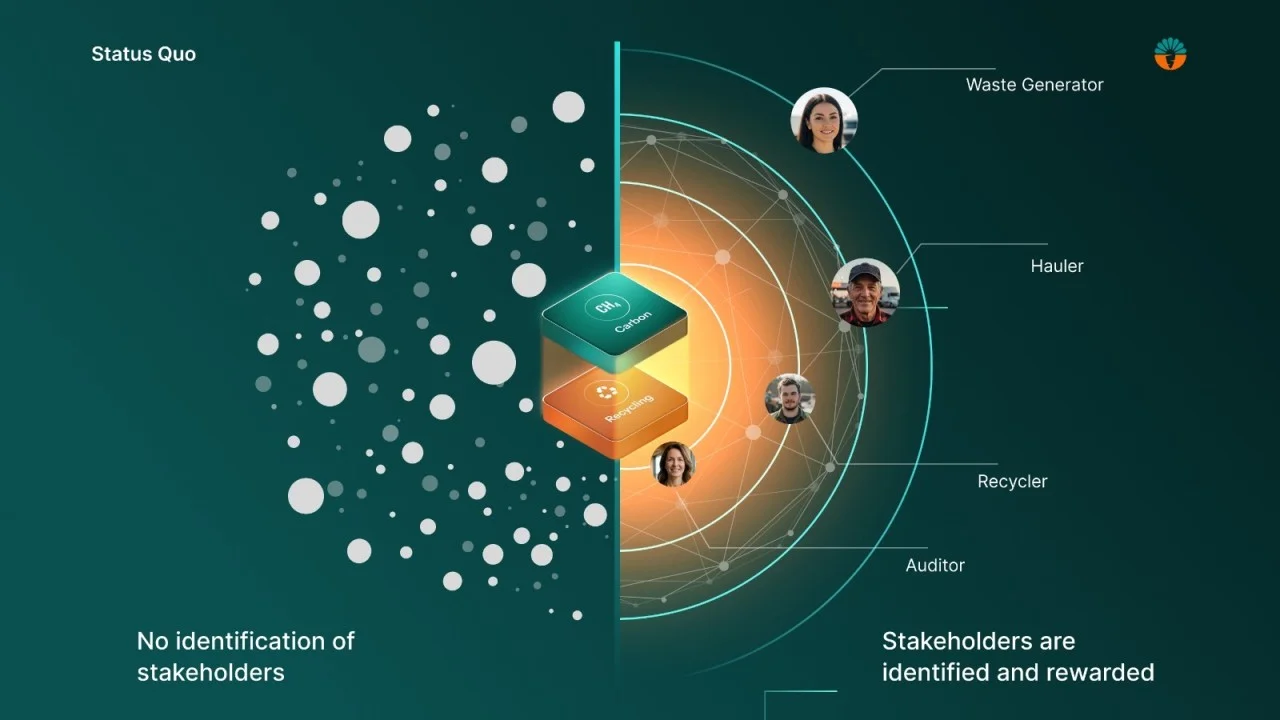

Waste systems are local, fragmented, and chronically mismanaged and underfunded. Cities want to divert organics but face near-term cost increases and political risk. Developers want to build treatment capacity but cannot finance it without predictable feedstock supply and a market to sell new products into. Corporate buyers want credible methane action but have few investible projects that can be scaled across jurisdictions. What has been missing is a financing architecture that connects the interventions we already know are necessary into a sequence that scales.

A Financing Roadmap Has Emerged

Over the past several years, and especially the last few months, a clear financing and policy roadmap has taken shape—a convergence of work across multiple organizations and geographies.

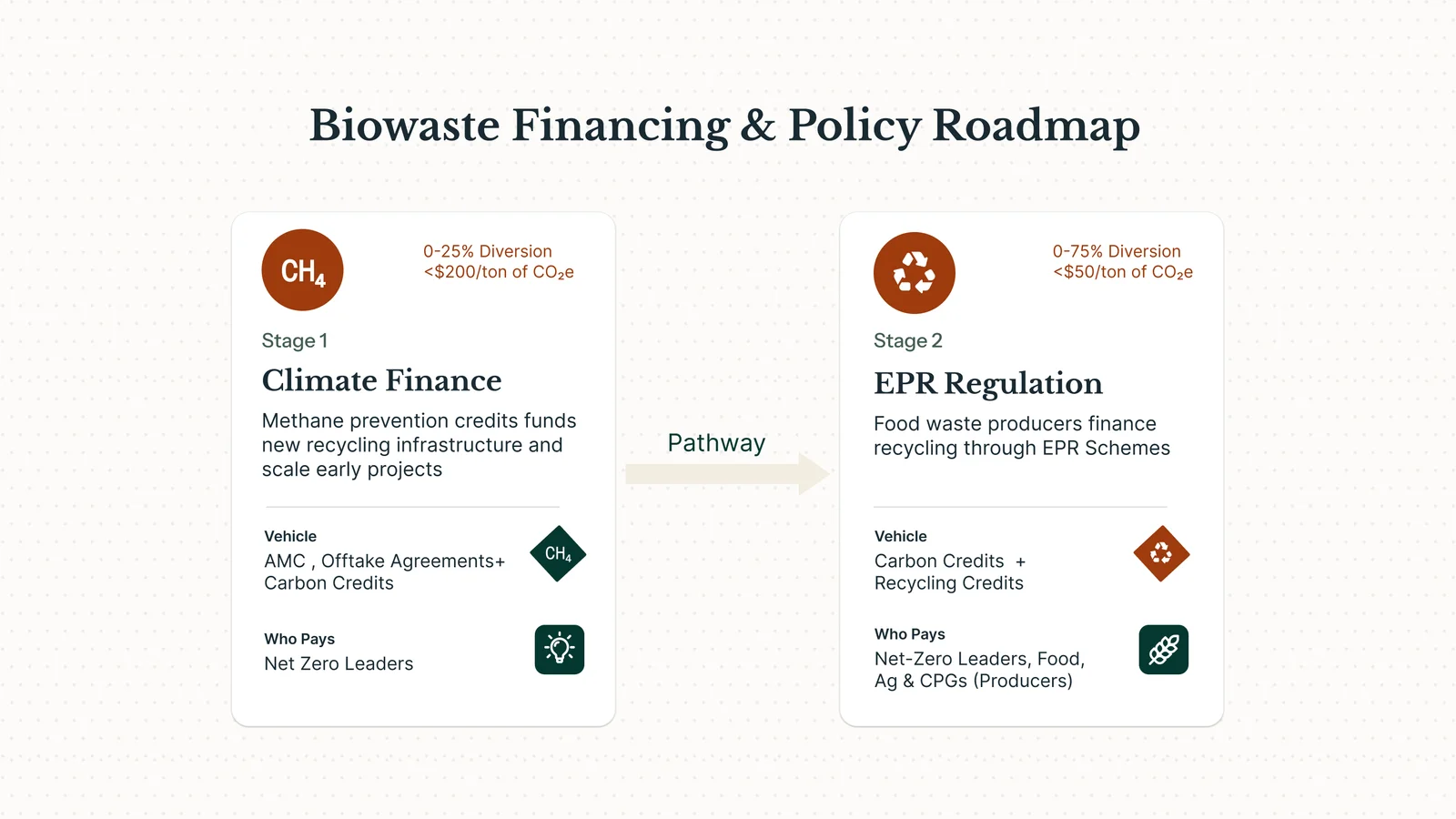

The roadmap has two catalytic phases that together form an unlocking mechanism:

As first presented at COP30 in the Super Pollutant Pavilion

Phase 1: Carbon Finance. Catalytic carbon credits fund the first wave of composting, anaerobic digestion, and other infrastructure and services. Anchor buyers — companies pursuing net-zero with methane exposure — make forward purchase commitments and direct purchases that give developers the revenue certainty needed to break ground and expand.

Phase 2: Food Extended Producer Responsibility (EPR). As infrastructure and services mature and verified diversion data accumulates, EPR regulation shifts funding responsibility to the food producers and consumer packaged goods companies that place waste-generating products into the economy. Biowaste recycling credits — purchased by producers to meet compliance requirements — create a durable, market-based revenue stream that sustains what carbon finance started. The participation base expands. The system becomes self-financing.

These phases are not speculative. The World Resources Institute described the framework for stacking environmental service payments as far back as 2009. Zero Waste Europe and the Bio-based Industries Consortium (BIC) published the policy case for Food EPR in January of this year, showing that financing needs to be sourced from food producers. Turkey, host country to COP31, has already launched the first Food EPR program. The Global Methane Hub is building national implementation plans. The Superpollutant Action Initiative—funded by the Big Techs and coordinated by Beyond Alliance—has signaled that corporate buyers are ready to invest in superpollutant mitigation. The science, funding, and political will are all now converging.

The question now is: what is the mechanism that connects Phase 1 to Phase 2 of the “Biowaste Roadmap”—that allows carbon finance to “Cold Start” the market while simultaneously pulling in the demand for EPR regulation to take effect?

The Biowaste Credit Stack

The Credit Stack is that mechanism.

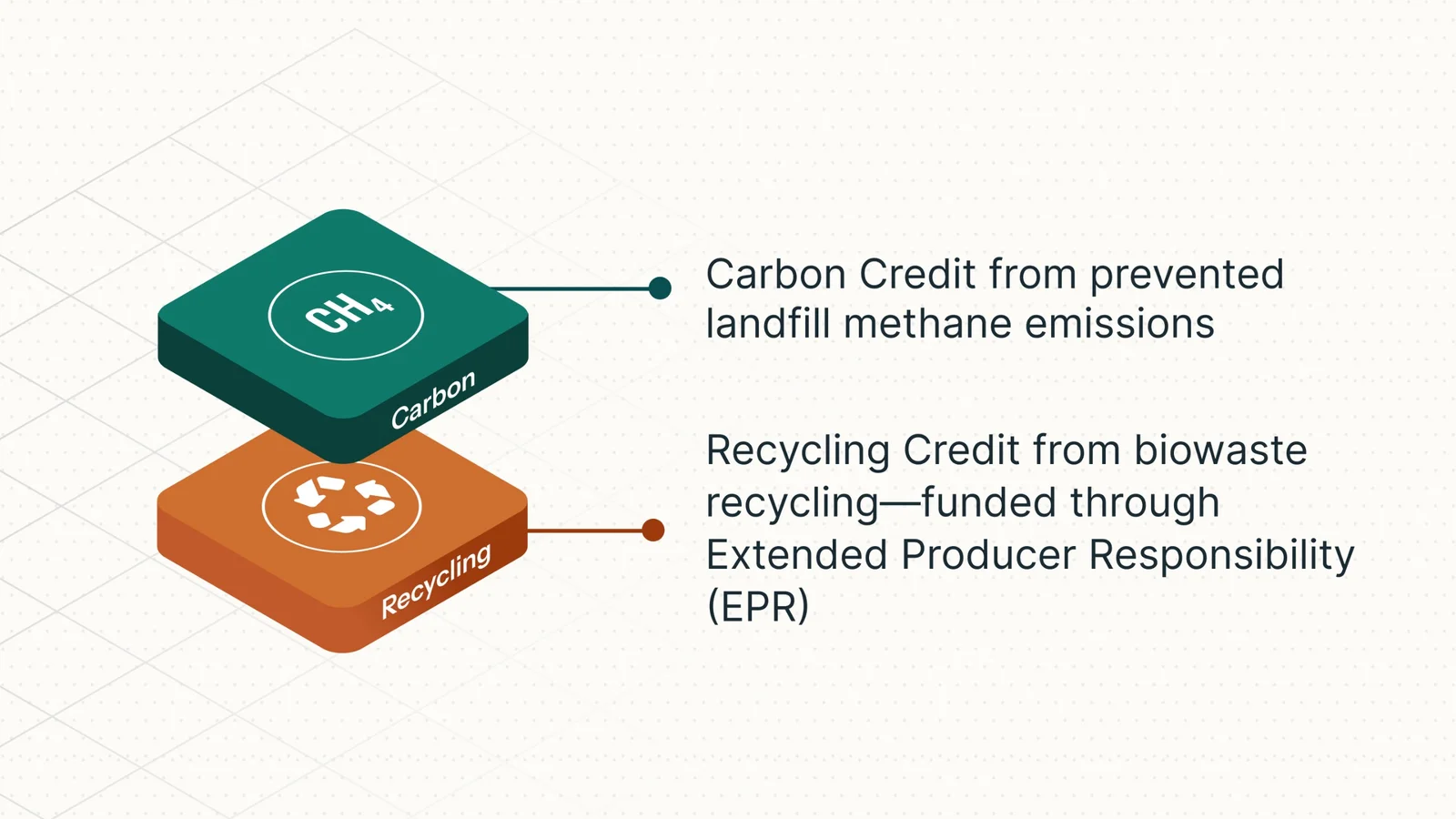

Here is how it works. When biowaste is diverted from a landfill and processed through a verified biological treatment facility, one certified waste mass unit creates two separate credits—each serving a different purpose based on the environmental impact it generated:

A carbon credit that represents the equivalent methane emissions prevented by diverting organic material from landfill burial.

A recycling credit that represents the verified recovery and biological treatment of that same organic material. This credit serves a recycling finance function: it proves that biowaste was properly diverted and processed, creating the compliance evidence that high-integrity Food EPR regulation requires.

The two credits are sold as a package, initially, but retired separately. This is the key design feature, and it matters for several important reasons.

It meets carbon credit buyers where they are. Carbon credit buyers are accustomed to purchasing credits that generate additional benefits beyond the carbon claim — but those benefits are rarely independently certified or separately retirable. The Credit Stack changes that: the recycling credit is not a co-benefit attached to the carbon credit. It is an independent environmental asset with its own methodology, its own verification, and its own market destination.

It cleanly delineates two separate utilities with no risk of double counting. Retired recycling credits make no claims on reduced methane emissions. Retired carbon credits make no claims over retired recycling benefits — or their associated co-benefits. Each serves a separate purpose: contributing to NetZero or methane reduction goals and biowaste diversion and recycling (EPR) objectives.

It commoditizes the credits. When each credit can function independently, they become standardized units that can be aggregated, compared, and retired at scale. This has practical consequences:

1. It enables investment in large portfolios of projects. Buyers and investors can spread capital across many facilities and geographies, reducing the risk associated with any single project. Portfolio-level investment is how capital markets scale.

2. It lowers the cost of participation for small and medium businesses. Being part of a portfolio enables small and medium companies (e.g., composters) to access capital, by participating in large crediting mechanisms even as small volume providers.

3. It enables the introduction of transparent Food EPR financing. When recycling credits are standardized, independently verifiable and retired in the voluntary recycling market, regulators have a mechanism to implement EPR. Producers can now purchase credits through independently verified, outcomes-based mechanisms rather than opaque, non-public producer-led schemes managed by PROs (Producer Responsibility Organizations). The funding base expands beyond early carbon buyers to include the industries generating the waste—all settled transparently.

4. Expanding participation reduces financing risk and creates a more resilient system. More buyers, more revenue streams (Carbon + Recycling), more geographies — the system becomes less dependent on any single funding source and becomes more durable over time.

It connects Phase 1 to Phase 2 in real time. In Phase 1, the carbon credit buyer purchases and retires both credits—funding the infrastructure and services needed while simultaneously building the verified diversion track record that Food EPR regulation needs to activate. As EPR takes effect, recycling credit demand shifts to mandated recycling claims (purchasing and retirement) by food producers. Carbon buyers are not locked in forever. They are catalysts—and the policy and system they helped build are what make the handoff possible.

The Concept Is Not New — the Execution Is

The idea of stacking payments for multiple ecosystem services from a single activity has been discussed for nearly two decades by the World Resources Institute, Duke University, and the OECD. The market even prefers stacking over bundling (Ecosystem Marketplace, 2024). What was missing was a clear execution opportunity and a policy roadmap.

That has now happened. The first stacked biowaste credits have been sold (by Carrot, in fact)—from the same verified waste mass, each retired separately, with independent third-party validation by Bureau Veritas Brasil mapped to the ICVCM’s core carbon principles.

Biowaste Diversion Completes the Portfolio

As carbon credit buyers expand their portfolios to tackle superpollutants and methane in particular, methane prevention through biowaste diversion adds a critical and complementary dimension. Landfill gas capture and destruction address emissions from waste already buried — essential work that should continue. But they do not stop new organic waste from entering landfills every day or the fugitive emissions, estimated at ~50%, that cannot be mitigated. Investing in biological treatment infrastructure and services shifts an industry toward methane prevention and controlled biogas production (anaerobic digestion) while building the circular economy systems that make destruction and capture less necessary over time.

Time for Action

The roadmap is clear, and the credit stack serves as a key enabler already fully functional within a voluntary market framework. Now it needs a coalition—buyers, policymakers, philanthropic supporters and implementers—willing to invest in building the circular biowaste treatment industry. The opportunity is here.

As Durwood Zaelke, one of the key architects of the Montreal Treaty that tackled the ozone layer, reminds us—there is an urgent ‘need-for-speed in tackling methane.’

If you want to discuss this opportunity for your organization, reach out. I’d welcome the conversation.